Could the FTHBI even be used in Toronto? INFOGRAPHIC

By Penelope Graham on Jun 27, 2019The First-Time Home Buyers Incentive, a new national mortgage-equity sharing program, has been the subject of sharp scrutiny since it was first announced by the federal government in March. Real estate and mortgage professionals have been questioning whether the new incentive, which will pony up a 5% to 10% loan for a down payment on a home, will actually have any teeth in Canada’s hottest markets due to its low income and purchase price eligibility thresholds.

Criteria too low to make a mark in hot markets

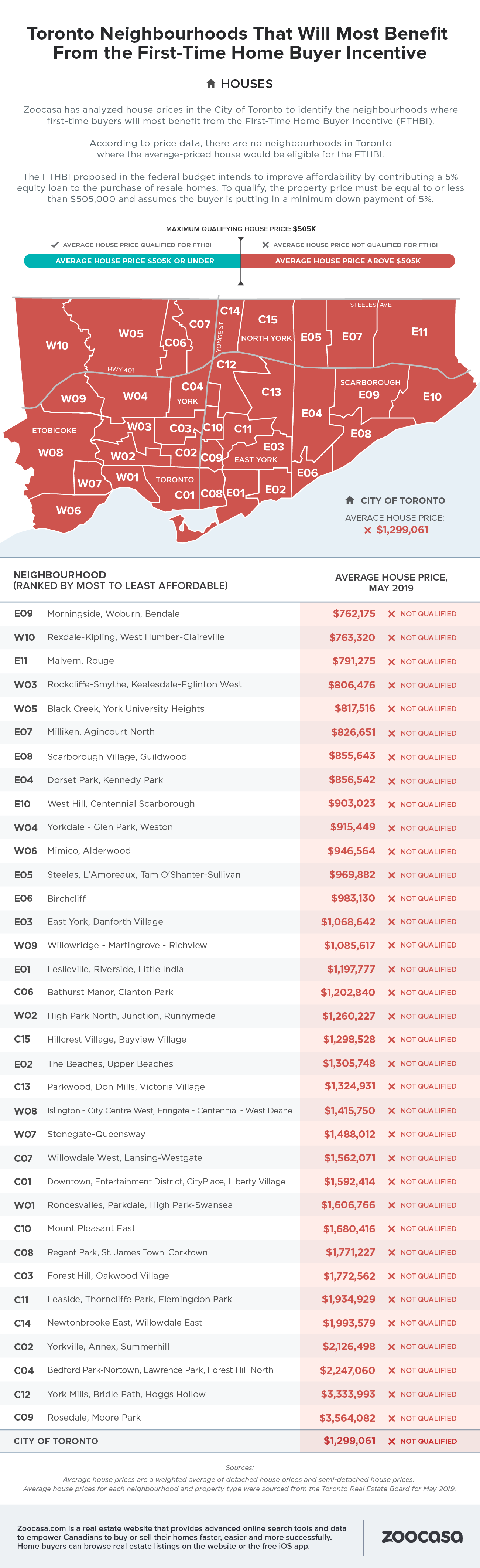

To participate in the FTHBI, prospective home buyers must satisfy a few restrictive criteria. First, they must be first-time buyers (or haven’t owned real estate within the last four years), and they must be able to qualify for a high-ratio (insured) mortgage from the Canada Mortgage and Housing Corporation, meaning they must have at least a 5% down payment saved.Where its effectiveness comes into question, however, is in regards to its mortgage and income requirements; buyers cannot have a combined household income of more than $120,000, and the mortgage cannot exceed more than four times that amount, at a maximum of $480,000. That means, should a buyer put the minimum 5% down and receive another 5% from the CMHC under the FTHBI, the most expensive home they could purchase would be limited to $505,000 – arguably a threshold that won’t get very far in a market like Toronto where the average home price exceeded $900,000 in May 2019.

First-time home buyers out of luck with FTHBI

So, would it be at all plausible for the FTHBI to be utilized in Toronto? A recent study conducted by Zoocasa reveals it’s possible – though options are limited. The study examined May average sold prices for both condos and houses in 35 MLS district neighbourhoods across the city, and assumes a buyer has the maximum income and a 5% down payment saved.It found that for those looking to purchase the average priced house (at a weighted average of both detached and semi-detached homes) have zero ability to use the program; there isn’t a single neighbourhood with eligible housing stock in the 416, as the average price sits at $1.2 million.

Options available for some condo buyers in city

However, condo buyers will be able to find options in 13 neighbourhoods, where the average price is low enough to be considered eligible under the FTHBI. They are generally located outside of the city’s core with the top three including:- West Hill, Centennial Scarborough (Average home price: $352,389)

- Malvern, Rouge (Average home price: $362,037)

- Black Creek, York University Heights (Average home price: $373,932)

Check out the infographics below to see where in Toronto the FTHBI may be utilized:

Penelope Graham is the Managing Editor at Zoocasa, a real estate website that provides advanced online search tools and data to empower Canadians to buy or sell their homes faster, easier and more successfully including condos in downtown Toronto, North York condos, and Etobicoke condos for sale. Home buyers can browse real estate listings on the website or the free iOS app.